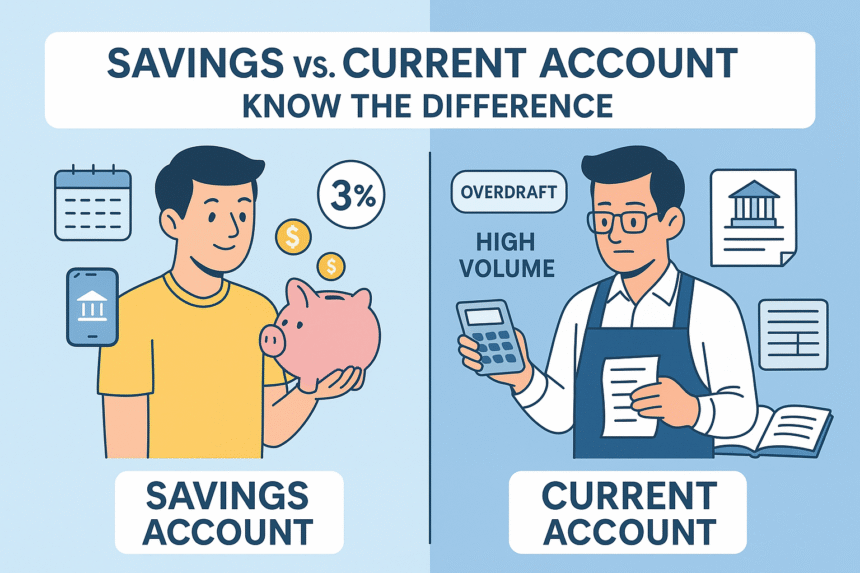

When it comes to banking, the most basic decision you’ll face is: Should I open a Savings Account or a Current Account?

This question seems simple, but it holds the key to how you manage your money, how much interest you earn (or don’t), and what banking facilities you can enjoy.

In this article, we’ll break down the difference between a savings account and a current account — with examples, use cases, and a handy comparison table — so that you know exactly which one suits your needs.

🏦 What Is a Savings Account?

A Savings Account is a type of bank account designed for individuals to park their money and earn interest on it. It’s ideal for salaried individuals, students, pensioners, or anyone who wants to save money over time.

✅ Key Features:

- You earn interest on the deposited amount (usually 2.5% to 4% p.a.).

- There’s a monthly/quarterly average balance requirement.

- You get a debit card, chequebook, passbook, and net/mobile banking access.

- Withdrawals are limited (to encourage savings).

- The account is mostly used for personal transactions.

🔍 Example:

Let’s say Ramesh, a school teacher, opens a savings account in SBI. Every month, his salary gets credited here. He keeps ₹50,000 as a balance. The bank offers 3% annual interest.

So, ₹50,000 x 3% = ₹1,500 per year as interest (before tax).

He also pays bills, transfers funds via UPI, and uses his debit card occasionally — all with ease.

🧾 What Is a Current Account?

A Current Account is a non-interest-bearing account mainly designed for business owners, professionals, firms, and companies that deal with high volume of daily transactions.

✅ Key Features:

- No interest is paid on the deposited balance.

- There’s no limit on withdrawals or deposits.

- The account usually requires a higher minimum balance.

- Facilities like overdraft, multi-location access, RTGS/NEFT priority handling, etc., are often available.

- Mainly used for business-related payments, not personal savings.

🔍 Example:

Seema owns a retail clothing store. She needs to pay suppliers, accept payments from distributors, and issue GST-related payments daily.

She opens a current account with HDFC Bank. Every day, transactions worth ₹2–3 lakh happen through her account. The bank gives her an overdraft limit of ₹1 lakh, which she uses during short cash crunches.

No interest is earned, but she enjoys speed, scale, and smooth handling of big payments.

⚖️ Savings Account vs. Current Account: At a Glance

| Feature | Savings Account | Current Account |

|---|---|---|

| Purpose | Personal savings | Business transactions |

| Interest | 2.5–4% per annum | No interest (in most cases) |

| Minimum Balance | ₹500–₹10,000 (varies by bank) | ₹5,000–₹1,00,000 or more |

| Transaction Limit | Moderate, with caps on withdrawals | Unlimited transactions |

| Overdraft Facility | Not usually available | Commonly available |

| Suitability | Salaried individuals, students, retirees | Businesses, firms, professionals |

| Bank Charges | Low or nil if minimum balance maintained | Higher, due to premium services |

| KYC Requirements | Standard personal KYC | Business KYC + Entity proofs |

💼 When Should You Choose a Savings Account?

Opt for a savings account if:

- You earn a fixed monthly income (salary, pension).

- You want to earn interest while keeping funds safe.

- You use banking for day-to-day personal expenses, not commercial use.

- You are a student, homemaker, or retiree.

- You do not need high-volume transactions.

💡 Pro Tip:

Many banks now offer zero balance savings accounts or salary accounts that waive minimum balance requirements. Some banks also offer savings accounts with sweep-in FD features, where excess money is moved to FDs automatically to earn more interest.

🧑💼 When Should You Choose a Current Account?

Choose a current account if:

- You run a business or are a self-employed professional.

- You need to issue or receive multiple high-value transactions daily.

- You want no restriction on withdrawals.

- You require overdraft facilities, cheque collection services, or special business tools.

- You want to separate your personal and business finances for better tracking and taxation.

💡 Pro Tip:

Banks often bundle POS machines, QR codes, SMS alerts, and accounting software integrations with current accounts to help businesses operate smoothly.

🤔 Common Confusions Cleared

❓ Can I open a savings and current account in the same bank?

Yes, you can. Many business owners have a savings account for personal use and a current account for their business— even in the same branch.

❓ Can I convert a savings account to a current account?

No, these are separate account types with different KYC and compliance requirements. You’ll need to close one and open the other.

❓ Which account is safer?

Both are equally safe as long as they are with RBI-regulated banks. However, only savings accounts up to ₹5 lakh are covered under DICGC insurance (including principal and interest).

🔚 Final Thoughts

A savings account is like a piggy bank with benefits — ideal for parking your salary, savings, and short-term goals.

A current account is a powerful business tool — allowing you the freedom to move large sums without friction.

The key is to choose what fits your purpose.

💬 “Money works best when it’s put in the right place — and that begins with choosing the right account.”

🧭 Bonus Tip: What Most People Miss

Many small business owners mistakenly use their savings account for business use — which can trigger compliance issues or account freezes. Always open a current account for any form of commercial activity.

📌 Quick Action Items:

- Already have a savings account? Check your interest rate and minimum balance rules.

- Running a side business or freelancing? Consider opening a separate current account.

- Not earning interest on your idle money? Explore auto sweep savings options.

Would you like a downloadable PDF version of this guide or want to embed a comparison calculator for your readers?

Let me know and I’ll help you with that too!

Blog Title:

Savings Account vs. Current Account – What’s the Real Difference? Explained with Easy Examples

When it comes to banking, the most basic decision you’ll face is: Should I open a Savings Account or a Current Account?

This question seems simple, but it holds the key to how you manage your money, how much interest you earn (or don’t), and what banking facilities you can enjoy.

In this article, we’ll break down the difference between a savings account and a current account — with examples, use cases, and a handy comparison table — so that you know exactly which one suits your needs.

🏦 What Is a Savings Account?

A Savings Account is a type of bank account designed for individuals to park their money and earn interest on it. It’s ideal for salaried individuals, students, pensioners, or anyone who wants to save money over time.

✅ Key Features:

- You earn interest on the deposited amount (usually 2.5% to 4% p.a.).

- There’s a monthly/quarterly average balance requirement.

- You get a debit card, chequebook, passbook, and net/mobile banking access.

- Withdrawals are limited (to encourage savings).

- The account is mostly used for personal transactions.

🔍 Example:

Let’s say Ramesh, a school teacher, opens a savings account in SBI. Every month, his salary gets credited here. He keeps ₹50,000 as a balance. The bank offers 3% annual interest.

So, ₹50,000 x 3% = ₹1,500 per year as interest (before tax).

He also pays bills, transfers funds via UPI, and uses his debit card occasionally — all with ease.

🧾 What Is a Current Account?

A Current Account is a non-interest-bearing account mainly designed for business owners, professionals, firms, and companies that deal with high volume of daily transactions.

✅ Key Features:

- No interest is paid on the deposited balance.

- There’s no limit on withdrawals or deposits.

- The account usually requires a higher minimum balance.

- Facilities like overdraft, multi-location access, RTGS/NEFT priority handling, etc., are often available.

- Mainly used for business-related payments, not personal savings.

🔍 Example:

Seema owns a retail clothing store. She needs to pay suppliers, accept payments from distributors, and issue GST-related payments daily.

She opens a current account with HDFC Bank. Every day, transactions worth ₹2–3 lakh happen through her account. The bank gives her an overdraft limit of ₹1 lakh, which she uses during short cash crunches.

No interest is earned, but she enjoys speed, scale, and smooth handling of big payments.

⚖️ Savings Account vs. Current Account: At a Glance

| Feature | Savings Account | Current Account |

|---|---|---|

| Purpose | Personal savings | Business transactions |

| Interest | 2.5–4% per annum | No interest (in most cases) |

| Minimum Balance | ₹500–₹10,000 (varies by bank) | ₹5,000–₹1,00,000 or more |

| Transaction Limit | Moderate, with caps on withdrawals | Unlimited transactions |

| Overdraft Facility | Not usually available | Commonly available |

| Suitability | Salaried individuals, students, retirees | Businesses, firms, professionals |

| Bank Charges | Low or nil if minimum balance maintained | Higher, due to premium services |

| KYC Requirements | Standard personal KYC | Business KYC + Entity proofs |

💼 When Should You Choose a Savings Account?

Opt for a savings account if:

- You earn a fixed monthly income (salary, pension).

- You want to earn interest while keeping funds safe.

- You use banking for day-to-day personal expenses, not commercial use.

- You are a student, homemaker, or retiree.

- You do not need high-volume transactions.

💡 Pro Tip:

Many banks now offer zero balance savings accounts or salary accounts that waive minimum balance requirements. Some banks also offer savings accounts with sweep-in FD features, where excess money is moved to FDs automatically to earn more interest.

🧑💼 When Should You Choose a Current Account?

Choose a current account if:

- You run a business or are a self-employed professional.

- You need to issue or receive multiple high-value transactions daily.

- You want no restriction on withdrawals.

- You require overdraft facilities, cheque collection services, or special business tools.

- You want to separate your personal and business finances for better tracking and taxation.

💡 Pro Tip:

Banks often bundle POS machines, QR codes, SMS alerts, and accounting software integrations with current accounts to help businesses operate smoothly.

🤔 Common Confusions Cleared

❓ Can I open a savings and current account in the same bank?

Yes, you can. Many business owners have a savings account for personal use and a current account for their business— even in the same branch.

❓ Can I convert a savings account to a current account?

No, these are separate account types with different KYC and compliance requirements. You’ll need to close one and open the other.

❓ Which account is safer?

Both are equally safe as long as they are with RBI-regulated banks. However, only savings accounts up to ₹5 lakh are covered under DICGC insurance (including principal and interest).

🔚 Final Thoughts

A savings account is like a piggy bank with benefits — ideal for parking your salary, savings, and short-term goals.

A current account is a powerful business tool — allowing you the freedom to move large sums without friction.

The key is to choose what fits your purpose.

💬 “Money works best when it’s put in the right place — and that begins with choosing the right account.”

🧭 Bonus Tip: What Most People Miss

Many small business owners mistakenly use their savings account for business use — which can trigger compliance issues or account freezes. Always open a current account for any form of commercial activity.

📌 Quick Action Items:

- Already have a savings account? Check your interest rate and minimum balance rules.

- Running a side business or freelancing? Consider opening a separate current account.

- Not earning interest on your idle money? Explore auto sweep savings options.